by senior futurist Richard Worzel, C.F.A.

At this stage in an economic cycle, inflation has usually reared its head, and the U.S. Federal Reserve (the Fed) is typically thinking about taking the punchbowl away from the (stock market) party by jacking up interest rates. In turn, this usually kills the economic recovery, tipping us over into recession.

But inflation has been notably, remarkably, absent, so much so that the Fed has consistently missed its inflation targets on the low side. Meanwhile, the presidents of the various regional Federal Reserve Banks (of New York, St. Louis, etc.) have been regulars on Bloomberg and other financial media, straining to explain what’s happened as inflation seems to have disappeared.

This has been bad news for gold bugs, as well as inflation and deficit hawks, some of whom have been forecasting inflation, serious inflation, or hyperinflation (and been notably wrong) since the bottom of the Great Recession in 2009-10. And yet, such commentators haven’t recanted; they still insist inflation is just around the corner.

I have a couple of thoughts about why inflation has gone away. I’m not an economist, but have been a keen student and user of economics for decades, starting with my university studies, then blending into my days working in the stock and bond markets.

In this vein, it occurs to me that there are at least three things going on that have contained inflation, and will continue to do so.

Demographics Is Keeping Demand Soft

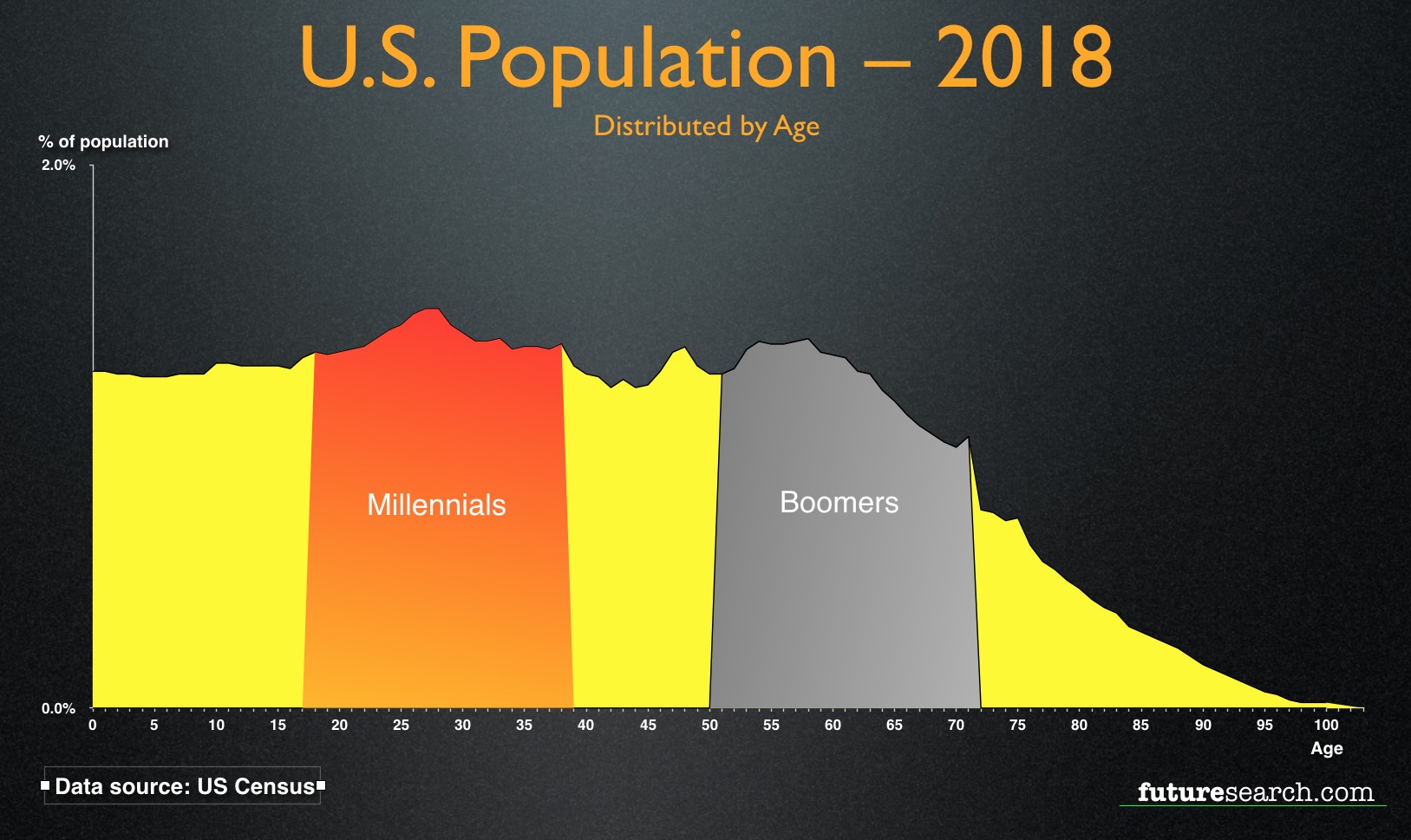

There have been a small number of studies relating inflation – and hence interest rates – to demographics. And although they’ve been rare, they have also been remarkably consistent, going back to the 1970s, when inflation began to run rampant.

The basic thesis is that younger people in the family formation stage of life tend to buy more stuff than older people in, or near to, retirement. And the baby boom, while gradually shuffling off-stage from the workplace, is still the second largest age group in the population, is also the wealthiest, and has the greatest economic clout. (Marketers seem to have forgotten Willie Sutton’s dictum by ignoring the boomers: when asked why he robbed banks, he remarked, “Because that’s where the money is.” But that’s another subject for another day.)

The boomers are, as I said, retiring, and while they are buying stuff related to retirement, such as travel and health care, they are not buying as many everyday possessions. They are largely in replacement mode rather than acquisition mode. So, they are buying less furniture, fewer clothes, they don’t commute so they don’t need as many (or as frequent) cars, and so on. And, as stock traders like to remark when asked why the stock market goes down on a given day, “More sellers than buyers.” When members of the richest generation with the greatest economic clout buy less stuff, demand will likely stay limp.

Of course, the generations below, notably the Millennials, are in the acquisition stage of their lives, but many of them are struggling financially, either because they haven’t been able to find suitable jobs (or no jobs at all), because they’re still paying off student loans, because they’ve delayed starting families, or some combination of these things.

So, the first factor I would point to is that demand is weak because not as many people are buying things.

Workers Are in Weak Bargaining Positions

Next is a factor mentioned in passing above: the job market. While many people of working age are well along in building their careers, a significant fraction are either frozen out entirely, and have been unemployed for more than a year, or are making do with entry-level or minimum-wage related jobs. This is especially true, again, of Millennials.

The exodus of manufacturing and related jobs is one major cause. The emergence of a global economy is gradually producing a leveling of wages for many kinds of work around the world. And since developed countries had the highest wages for unskilled and semi-skilled wages, they have been hit the hardest.

But that’s old news. What is newer news is the mushrooming expansion of automation. My colleague, Kit Worzel, and I have talked about this at length here and here. Therefore, let me just sum this up by saying that smart computers, including those using Artificial Intelligence, are leading to more capable automation and robots to augment or replace human workers. And as AI improves at computer-related speeds, automation is going to eat its way up the food-chain very quickly indeed.

Automation does not need to replace the workers of an entire industry, category of jobs, or the economy as a whole in order to have a severe dampening effect on wages. The Economist news magazine explored a parallel example based on the analysis of British economist Tim Harford.

My interpretation of Harford’s work would be that job-seeking becomes like a game of musical chairs as automation steadily removes jobs from the workplace. Even if the rate at which we lose jobs to automation is slight, the knock-on effects can be significant as it disproportionately reduces the bargaining power of all job seekers.

I realize this is an oversimplification of the very complex economics of employment, but it would explain why wage demands remain weak, even as the economy reaches what most would describe as full employment.

And when you add the changing nature of jobs, the argument becomes even more compelling. Even though the number of jobs is rising, the quality of many of the jobs created seems, on average, to be declining. You can see this in the research on the contingent labor force, and the anecdotes of people having to work two- and three part-time jobs to make ends meet after having lost higher-paying, full-time jobs. And, of course, as I mentioned earlier, lower incomes lead to lower consumption, plus delayed household formation for many Millennials.

So, my second factor leading to low inflation is that workers are, on average, losing bargaining power, even in what appears to be a buoyant economy.

Weak Corporate Investment

There are three principal players in the economy: consumers, corporations, and governments. So far, we’ve explored why consumer demand appears to be weak. Now let’s look at corporations.

There are two things happening in the corporate world that weaken corporate demand. First, weak consumer demand means that there’s very little need or impetus to invest in new plant and equipment. When you can meet demand with your existing infrastructure, or by adding a second shift to your workforce, then there’s very little appetite to buy equipment to increase production. We’re clearly seeing that.

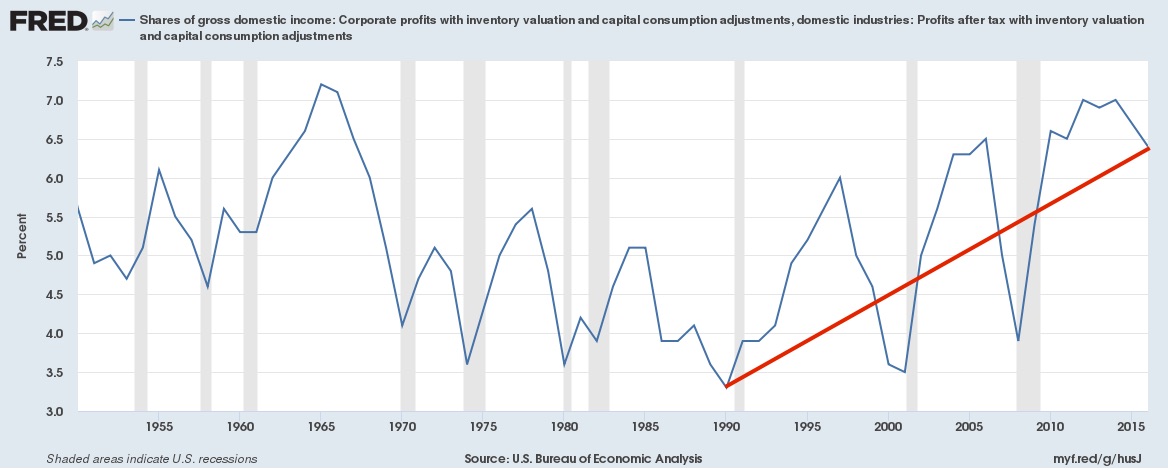

And, just as the introduction of automation limits the bargaining power of workers, it also increases the bargaining power of management and owners. This, too, is quite evident in the steadily rising share of economic activity (GDP) accruing to profits rather than to workers, as seen below in the two graphs below from Federal Reserve Economic Data (FRED) produced by the Federal Reserve Bank of St. Louis. For both graphs, I’ve added a red line connecting the years 1990 and 2016 to better illustrate the changes:

Share of GDP due to Employee Compensation, 1950-2016

And here’s the share due to profits. The deep drops in profits are due to recessions:

Share of GDP due to Corporate Profits, 1950-2016

So, corporations have money to invest; the corporate sector is awash in cash balances right now. It’s just that they have little or no motivation to spend that cash. So, except where there is a desire to replace or supplement workers with automation, robots, or cobots, businesses have little reason to invest, and hence, corporate demand shows up as surprisingly weak for this stage of an economic cycle.

What Happens Next? And Why Does It Matter?

I don’t see significant changes occurring in any of these three factors soon. I do expect that as labor markets continue to tighten, wages will start to firm up slightly. But, it also seems to me that as quickly as wage demands start to rise, corporations will introduce more automation, knocking wages back down again.

Of course, that will lead to some increase in corporate investment. But overall, I suspect these two changes will have a relatively small effect on the overall rate of inflation, less than most economists are likely to project.

I expect, therefore, that although inflation may rise slightly, and interest rates with it, I don’t expect either to rise dramatically – unless there’s some unexpected crisis. And low inflation is generally a good thing.

However, continuing low inflation also means continuing low interest rates, and hence the continued, and potentially dangerous, growth of asset bubbles, as is going on in the stock market right now. As well, the weak wage situation of workers means that consumer debt is high, which may well carry the seeds of the next recession.

Meanwhile, the thing that corporations appear to have overlooked in the rosy outlook for corporate profits is that if workers don’t have money to spend, then neither do consumers, for they are essentially the same group.

Henry Ford understood this, which is why he raised the wages of his assembly-line workers so that they could buy Ford’s cars. That lesson seems arcane and lost in the mists of antiquity today, but will come back to bite us.

© Copyright, IF Research, January 2018.